Actually, Lease to Own Cars Malaysia is becoming a go-to option because it prioritizes immediate use over long-term debt commitment. It’s a practical “middle path” for those who need a reliable car but don’t want to deal with the rigid walls of traditional bank approvals. Whether you’re a family in Penang or a startup in KL, the focus here is on flexibility and cash flow management.

- 1️⃣ Lease-to-own avoids the rigid “lock-in” and strict scoring of traditional bank loans

- 2️⃣ Business owners use leasing as an operating expense to preserve essential capital

- 3️⃣ Monthly payments cover insurance and road tax to provide total peace of mind

- 4️⃣ Modern digital tools ensure transparency for the entire journey toward ownership

Why the old way of buying a car feels so ‘leceh’ now

So that’s how it works: the traditional hire-purchase model is getting harder for the average person. Simply put, banks have become much stricter with their “scoring.” You might have a decent job in Kuala Lumpur, but if your PTPTN is a bit messy, getting a loan is hard. Furthermore, if you’ve just started a new business, getting that 90% loan is like trying to find parking in Mid Valley on a Saturday—nearly impossible.

What many people don’t realize is that owning a car isn’t just about the monthly installment. When you take a 9-year bank loan, you are basically “locked in.” If your life situation changes, selling a car that is still under a heavy bank loan can be a nightmare. Specifically, you might have to pay a “top-up” to the bank because the car’s value dropped faster than the loan balance.

In a Lease to Own Cars Malaysia setup, the vibe is different. It feels more like a long-term subscription with an option to keep the car at the end. For many office workers, it takes away the “pening” (headache) of maintenance and depreciation risks. Consequently, you get to drive the car you need today. If your financial situation improves in three years, you have more options than someone stuck in a rigid 108-month contract.

The shift in how local bosses view company cars

To be frank, if you’re running a small business in Johor Bahru or Selangor, tying up your capital in a fleet of cars is probably the last thing you want to do. I’ve seen many “taukes” struggle because they put all their cash into downpayments. Consequently, they find they don’t have enough “pusing” (rotation) money for their monthly stock or payroll.

Actually, Lease to Own Cars Malaysia is a strategic move for cash flow. Instead of showing a huge liability on the balance sheet, it’s treated more as an operating expense. This keeps the company’s credit lines “cantik” for when they actually need to borrow money for big things. For instance, they might need funds for expanding their warehouse or buying new machinery.

In situations like this, organizations such as R Global usually only play a supportive, administrative, or neutral assistance role. They aren’t there to act like a traditional car salesman trying to hit a quota. Instead, they handle the heavy lifting of the documentation and registration. This makes the process much smoother for the business owner. Therefore, they can focus on getting the car on the road as fast as possible so the business can actually start making money.

Breaking down the real costs and requirements

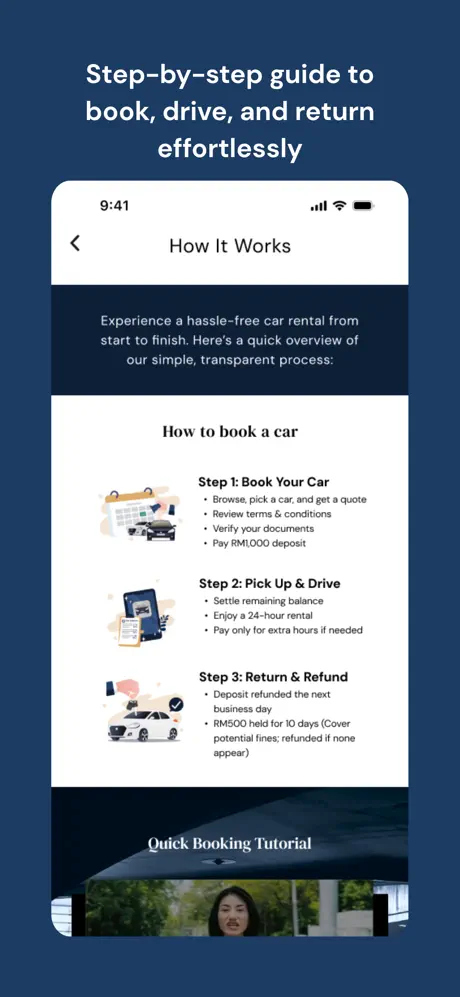

What many people get wrong is thinking that “lease to own” means “cheap.” Honestly, it’s not necessarily about being the cheapest option. Instead, it’s about the total value and the “convenience fee.” You have to look at the costs of Lease to Own Cars Malaysia as a package. Usually, the monthly payment might look slightly higher than a bank loan, but you have to remember what’s included inside that “bungkus” (package).

Simply put, you are often paying for peace of mind. Things like road tax, insurance, and even basic service maintenance are often bundled in. If you add up the “hidden costs” of a traditional loan, the gap starts to close. Moreover, the requirements for Lease to Own Cars Malaysia are generally more relaxed than a bank. Usually, providers care more about your current ability to pay rather than your history from five years ago.

Here is a quick look at how the typical scenarios play out for different types of drivers:

- Upfront Cost: Usually involves a security deposit rather than a 10-20% downpayment.

- Documentation: Simple IC, license, and basic proof of income (even for self-employed).

- End-of-Term: You can choose to pay a small residual value to transfer the name or just return the car.

— Image sourced from the internet

The new lifestyle of “Car Subscribing” in 2026

Looking at the current landscape, the “subscription” mindset is really taking over. People are realizing that they don’t need to “own” the headache of a depreciating asset. Instead, they just want the utility of the car. It’s the same reason we use Grab—we want the ride, not necessarily the car itself. Consequently, Lease to Own Cars Malaysia providers are growing fast.

What’s interesting is how technology is making this even easier. Nowadays, you don’t even have to walk into a physical office to check your status. Most modern providers are integrating everything into digital platforms. For instance, the Car Dreams App has become a very handy tool for people to track their journey toward ownership. It allows users to see exactly how much they’ve paid. Moreover, you can see when the next service is due. It’s all about transparency—no more “agak-agak” (guessing) about where your money is going.

Even for R Global, the goal is to keep things moving in the background. At the end of the day, whether you are driving through the heavy rain in Subang or cruising along the coast in Penang, you just want to know that your transport is settled. The market is shifting toward these more human-centric models because, frankly, life is complicated enough. We don’t need our cars to be another source of stress. Therefore, we expect Lease to Own Cars Malaysia to remain a top choice for the years ahead.

Honestly, it’s quite a relief to see that we have more options now compared to ten years ago. Back then, it was “bank loan or nothing,” and if you didn’t fit into their narrow box, you were stuck taking the bus or riding a bike in the hot sun. Now, with lease-to-own becoming more common, there’s a sense that anyone who works hard can get behind the wheel. It’s just a more inclusive way of doing things. I’ve seen friends who finally managed to get a decent car for their growing families through this method, and the smile on their faces when they don’t have to worry about a “rejected” letter from the bank—that’s the real win.

R Global Luxury Car Rental Contact Information

Official Website: rglobalcarrental.com

Email Address: lucas@rglobalcar.com

Phone Number: +60 11-1093 3319

Car Dream App:

Download on Google Play

Download on App Store

R Global Luxury Car Rental Branch Information (Malaysia)

| Region | Address |

| Johor Bahru (JB) | 89a, Jalan Persisiran Perling, Taman Perling, Johor Bahru, Johor, 81100, Malaysia |

| Kuala Lumpur / Selangor (KL) | SO-G-12, Jln Equine, Taman Equine, 43300 Seri Kembangan, Selangor |

| Penang | 1-9A-01, Lintang Mayang Pasir 1, Bandar Bayan Baru, Pulau Pinang, 11950, Malaysia |

| Kota Kinabalu, Sabah | Lorong Api Api, Kota Kinabalu, Sabah, 88000, Malaysia. |

| Kuching, Sarawak | Green Heights Commercial Centre, Kuching, Sarawak, 93250, Malaysia. |

💬 2026 Mobility FAQ: Which Path Fits You?

Real-world concerns for fresh grads, expats, and business owners in 2026.